Climate Change Crisis

Commitment

Aiming to achieve Net Zero by 2050, Thai AirAsia has set goals to progressively intensify its environmental management policy on a yearly basis.

The Company’s policies, operations and adoption of new technologies and know-how are all geared towards minimising and controlling the greenhouse gas emissions (GHG) into the atmosphere.

Net Zero Strategy

The Company is committed to conducting its business to achieve net zero greenhouse gas emissions by 2050. As part of this commitment, the Company has strengthened its short-term target for 2026, focusing on reducing carbon dioxide emissions per available seat-kilometer by 1.5 gCO2/ASK compared to 2025, and aims to achieve continuous reductions at the same rate each year thereafter.

2025 Performance

In 2025, the Company targeted 69 gCO2/RPK of carbon dioxide emissions per revenue passenger kilometre. However, the rate for the year was 77.4 gCO2/RPK.

The increase in CO2 emissions from the prior year was reflecting a shift in our operational profile. While international flight frequencies decreased, there was a significant expansion in domestic operations. This change in the network mix resulted in higher overall fuel consumption, as shorter domestic sectors involve more frequent take-off and climb phases, which are the most fuel-intensive stages of flight.

Thai AirAsia Carbon Intensity

| Year | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|---|

| CO2 Emission per Available Seat Kilometre (CO2/ASK) | 66.5 | 69.0 | 72.8 | 66.6 | 64.2 | 64.0 | 63.0 |

| CO2 Emission per Revenue Passenger Kilometre (CO2/RPK) | 79.1 | 93.1 | 107.2 | 79.5 | 72.7 | 72.0 | 77.4 |

Short-Term Goal

Long-Term Goal

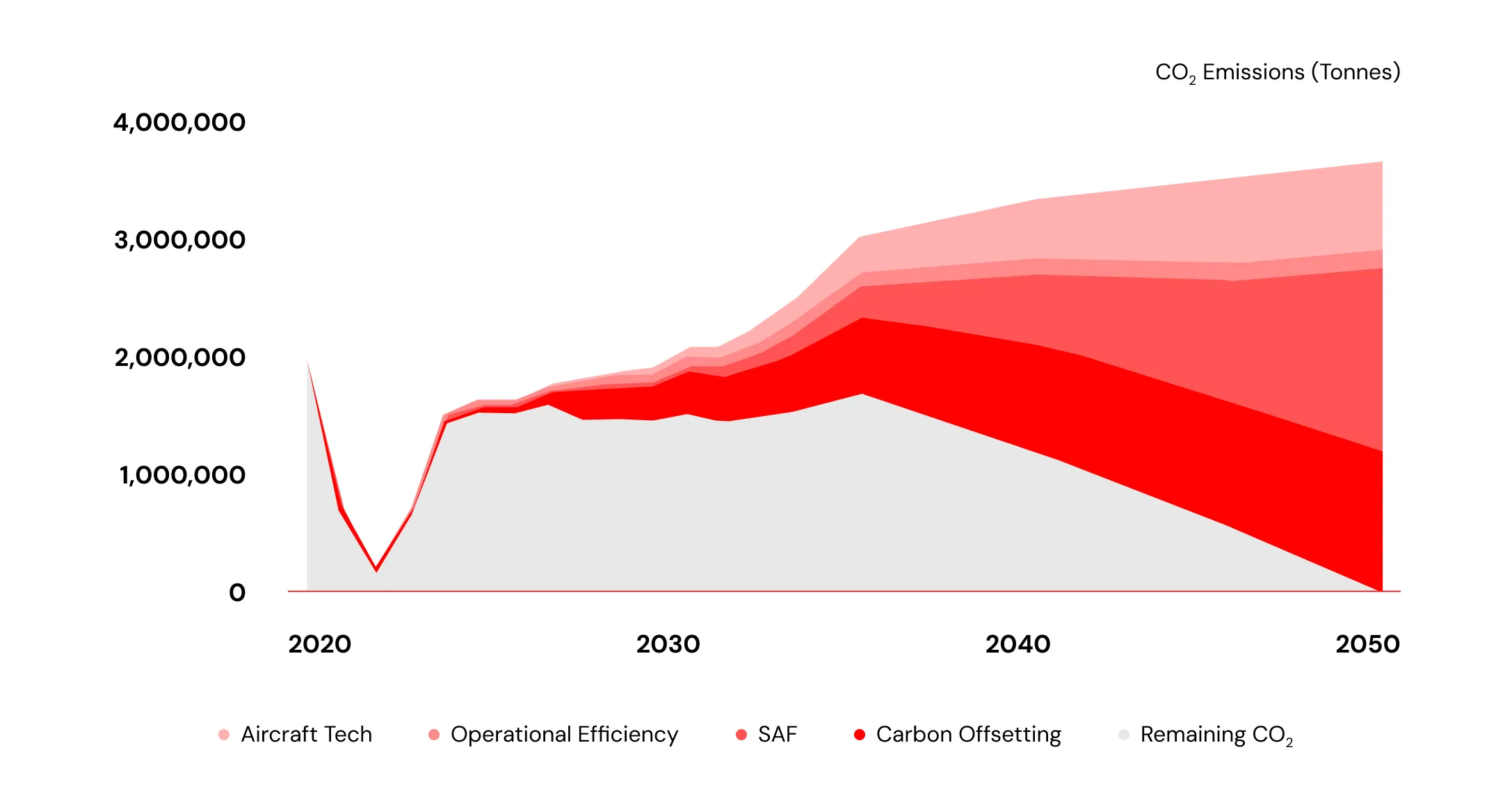

Roadmap Towards Net Zero by 2050

Thai AirAsia's 4 Key Pathways to Net Zero Emissions

1. Fleet Management

In 2025, Thai AirAsia took delivery of two A321neos for fleet expansion purposes. No aircraft were retired from the fleet. The average age of TAA rose slightly from 10.5 to 11.1 years as at 31 December 2025.

From Bangkok, these new aircraft models are expected to allow Thai AirAsia to reach new destinations in West Asia and Central Asia with a more fuel efficient option than widebody alternatives as these are expected to be new developmental routes.

For replacement of its A320ceo fleet, AirAsia is currently assessing two regional jet models with a five-hour flight range and 160 seat capacity. These regional jets will enable both more efficient flying and allow Thai AirAsia to rightsize to reduce excess capacity on some domestic and regional routes. The fleet replacement plan will also enable gradual lowering of fleet age upon its expected induction from 2028 onwards.

To enhance fuel efficiency, all new aircraft will be equipped with all-economy class and lightweight seats. New aircraft will also be pre-installed with software that allows implementation of our advanced fuel efficiency programme.

2025 Fleet Distribution

A320ceo

A320neo

A321neo

2. Operational Efficiency

Throughout 2025, Thai AirAsia continued strengthening its long-standing flight efficiency programme to reduce emissions at source. In total, TAA operated 12 green operating procedures further enhancing flight efficiency.

Operational Eco-Efficiency

The Average amount of Reduced CO2 from each Procedure

Performance

| No. | Key Operational Efficiency Measure | Thai AirAsia Implementation Rate | 2025 Fuel Savings (Tonnes) | 2025 Emissions Avoided (Tonnes of CO2) | ||

|---|---|---|---|---|---|---|

| 2023 | 2024 | 2025 | ||||

| 1 | Opti Climb | 76% | 66% | 63% | 4,856 | 15,345 |

| 2 | Single Engine Taxi - Departure | 44% | 47% | 48% | 1,536 | 4,854 |

| 3 | Single Engine Taxi - Arrival | 100% | 86% | 86% | 803 | 2,538 |

| 4 | Reduced Flaps Landing | 99% | 99% | 98% | 971 | 3,068 |

| 5 | Idle Reverse Landing | 99% | 100% | 99% | 678 | 2,143 |

| 6 | Packs OFF Take-Off | 100% | 94% | 97% | 266 | 841 |

Our Pilots Fly “Safe and Save”

Data: 2025

3. Sustainable Aviation Fuel

Thai AirAsia signed a Memorandum of Understanding (MOU) with the Civil Aviation Authority of Thailand (CAAT) on 17 November 2025 alongside seven other Thai carriers to promote the use of Sustainable Aviation Fuel (SAF). The agreement sets a target of 0.5% to 1% of SAF volume ratio on international flights from 2026 onwards, making a critical step towards achieving the industry’s Net Zero by 2050 goal.

The transition to SAF follows extensive consultation with the Ministry of Energy, CAAT, and industry partners. Before the formalisation of the SAF MOU, we participated in several foundational initiatives to ensure industry readiness:

- Sector Transition Workshops: Engaged in the "Thai Aviation Sector: Transitioning to SAF" seminars to align on the national energy roadmap.

- Quarterly SAF Working Groups: Active participation in recurring sessions with CAAT and domestic fuel producers to address supply chain logistics and feedstock security.

- Policy Alignment: Ongoing dialogue to establish a unified industry position on blending mandates and cost-sharing frameworks ahead of the 2026 mandate

4. Acquisition of Carbon Offsetting Credits

Thai AirAsia was instrumental in advocating for a carbon pricing mechanism that allows airlines to integrate CORSIA costs into airfares. In addition to engagements with CAAT, we organised information sessions for members of the Airlines Association of Thailand (AAT) to develop a unified industry position and recommend supportive policies to address Carbon Emission Unit (CEU) supply shortages. This culminated in regulatory approval for Thai carriers to introduce transparent carbon surcharges to airfares starting in 2026. This establishes a sustainable pathway for the industry to offset decarbonisation costs and mobilise funding to support its climate transition goals.

Additionally, direct engagement with the Thailand Greenhouse Gas Management Organization (TGO) has highlighted the urgent need for Thai airlines to comply with CORSIA standards, emphasizing risks associated with carbon credit shortages and rising costs. Discussions also promoted the integration of T-VER Premium carbon credits into ICAO-approved Eligible Emissions Units, ensuring that local projects meet international standards and provide a practical pathway for the aviation sector’s commitments.

Greenhouse Gas Emission Data

| Scope | Emission Type | Indicator | Source |

|---|---|---|---|

| Scope 1 | Direct emission | Fuel usage | Flight and ground operations |

| Scope 2 | Indirect emission | Electricity usage (Offices) | Electricity purchases |

| Scope 3 | Other indirect emissions | Fuel usage | GHG Protocol Scope 3 Category 3: activities involving fuel and energy and Category 6: business travel |

Scope 1 Emissions

| Scope 1 from Flight and Ground Operations | 2023 | 2024 | 2025 |

|---|---|---|---|

| GHG emissions from Domestic Flight (Tonnes of CO2) | 620,249 | 683,807 | 789,385 |

| Total GHG emissions from International Flight (Tonnes of CO2) | 811,312 | 901,301 | 837,087 |

| GHG emissions from ground operations (Tonnes of CO2) | 3,070 | 3,961 | 3,776 |

Note:

- In 2025, the Company enhanced its Scope 1 greenhouse gas emissions reporting for 2023–2025 by including emissions from ground operations, which were not included in the previous reporting.

- The increase in Scope 1 emissions is primarily driven by the expansion of domestic flight operations.

- The Company’s greenhouse gas emissions have been verified by the Management System Certification Institute (Thailand) (MASCI), an affiliate of the Foundation for Industrial Development. The verification covers fuel consumption and carbon dioxide emissions reports under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) regulations.

Scope 2 Emissions

| Scope 2 from Electricity Usage | 2023 | 2024 | 2025 |

|---|---|---|---|

| Electricity usage (kilowatt hours) | 4,003,543 | 4,369,595 | 4,024,156 |

| GHG emissions (Tonnes of CO2) | 1,726 | 1,923 | 1,690 |

Note:

The disclosure of Scope 2 emissions by Thai AirAsia covers emissions associated with energy usage at its Don Mueang hub and AirAsia Academy (other hubs and stations are not included). Evaluations and estimates of emissions are in accordance with TGO standards.

Scope 3 Emissions

| Scope 3 from upstream jet fuel production by suppliers and employee business travel | 2023 | 2024 | 2025 |

|---|---|---|---|

| GHG emissions (Tonnes of CO2) | 309,122 | 332,007 | 341,058 |

Note:

- Figures for 2024 have been restated to reflect refined data collection methodologies and improved data accuracy.

- The increase in Scope 3 emission in 2025 is a result from higher upstream emissions from the production, transport, and distribution of fuels, correlating with increased flight frequencies and operations.

Other Greenhouse Gas Emission

In addition to GHG emissions, the combustion of jet fuel releases nitrogen oxides (NOx), sulphur oxides (SOx), carbon monoxide (CO) and volatile organic compounds that affect the quality of air.

Over the years, improved engine designs have gradually reduced emissions of other GHGs. Under Annex 16, Volume III of its international standards on environmental protection, ICAO has set acceptable levels of emissions from aircraft engines for such gases.

In compliance with these standards, we strive to maintain a young fleet of aircraft that use the latest technologies. As of 2025, all AirAsia aircraft engines meet the most stringent ICAO CAEP/8 NOx emissions standards. As we continue to phase out older aircraft in exchange for new Airbus A321neo models, we aim for 100% compliance with ICAO CAEP/8 NOx standards.

| Other Greenhouse Gas Emissions | 2023 | 2024 | 2025 |

|---|---|---|---|

| NOx emissions (tonnes) | 868 | 1,200 | 1,415 |

| NOx emissions intensity (gNOx/RPK) | 0.043 | 0.06 | 0.07 |

| SOx emissions (tonnes) | 93 | 92 | 109 |

| Volatile Organic Compounds (VOC) emissions (tonnes) | 320 | 320 | 377 |

Note:

- NOx emissions and compliance data are obtained from the ICAO Emissions Bank issue 28C dated 20 July 2021. The NOx emissions value per landing and takeoff (LTO) cycle is based on the weighted average of AirAsia’s fleet composition as of 2024.

- According to the US EPA, SO2 represents the highest composition of SOx emissions, hence SO2 is considered as SOx for the purpose of calculations. SO2 and VOC emissions data are sourced from US EPA’s Generic Aircraft Type Emission Factors table.

- Figures for 2024 have been restated to reflect refined data collection methodologies and improved data accuracy.

Climate Financing

Thai AirAsia recognizes the growing significance of climate-related risks and opportunities as climate change continues to intensify. The Company is therefore committed to strengthening its capabilities in systematically managing potential impacts on both operations and financial performance.

Management Approach

- Risk Assessment and Preparedness

- Operational Foundation: The Company initiated a structured climate risk assessment process in 2023, aligned with the framework of the Task Force on Climate-related Financial Disclosures (TCFD). This includes the assessment of physical risks, transition risks, and opportunities that may impact the aviation industry across the short, medium, and long term. The objective is to evaluate financial implications and establish appropriate management strategies to enhance business resilience.

- Financial Analysis through Carbon Modelling: Since 2024, the Company has developed a carbon modelling tool to project climate-related costs over a five-year horizon. This is complemented by the adoption of internal carbon pricing, benchmarked against global carbon market prices and relevant regulatory considerations. These tools support financial impact forecasting and the integration of climate-related considerations into financial planning, investment decision-making, and capital allocation across all time horizons.

- Advancement towards International Standards (IFRS S2): The Company is currently conducting a gap analysis to assess the readiness of its climate-related data and processes in alignment with IFRS S2: Climate-related Disclosures. In addition, the Company plans to undertake climate scenario analysis under the IFRS S2 framework to evaluate the resilience of its business strategy under various global temperature pathways.

- Carbon Surcharge Implementation Thai AirAsia, in collaboration with the Airline Operators Association of Thailand, has engaged with the Civil Aviation Authority of Thailand regarding the implementation of a carbon surcharge. Approval has been granted for implementation on international routes operated by Thai carriers starting 1 January 2026. Proceeds from this carbon surcharge will be allocated to support the use of Sustainable Aviation Fuel (SAF) and/or the procurement of carbon credits.

Plan for 2026

As Thai AirAsia enters 2026, our climate strategy transitions from foundational planning to active execution. We are navigating a more complex regulatory environment characterised by the start of compliance carbon offsetting and the first operational requirement for SAF.

-

CORSIA Phase 1: Meeting Global Obligations

The year 2026 marks a pivotal moment for our international operations as we begin the first compliance cycle for CORSIA Phase 1 (2024–2026). Following the verification of our 2025 international emissions, Thai AirAsia is calculating its inaugural offsetting obligations.

-

Sustainable Aviation Fuel (SAF) Implementation

Following the Memorandum of Understanding (MOU) signed with the Civil Aviation Authority of Thailand (CAAT) in late 2025, Thai AirAsia is now focused on operationalising its SAF commitments. We will work closely with CAAT and domestic energy producers to mitigate the "green premium" costs typically associated with imported alternative fuels.

-

Financial Sustainability

To balance our environmental ambitions with our "Low Cost" DNA, we are introducing a transparent mechanism to fund these green transitions.

- Launch of Carbon Surcharge: To mitigate financial risks, Thai AirAsia collaborated with the government and the Airlines Association of Thailand to establish a carbon surcharge framework, which received formal approval in 2025. Collection of carbon fees is expected to begin in 2026

- Public Awareness & Advocacy: Ahead of the rollout, we are launching a nationwide campaign to educate guests on how these modest contributions directly support carbon reduction and our shared responsibility for the environment

-

Our public position

In coordination with AirAsia Group, we are managing emissions through a younger, more fuel-efficient fleet and expanded operational efficiency programmes. Our technological roadmap is further strengthened by the AirAsia-Airbus SAF research partnership, focusing on the regional integration of sustainable fuels. Simultaneously, we are deepening our engagement with state agencies and regulatory bodies via the Airlines Association of Thailand (AAT) to ensure that evolving climate regulations remain both environmentally effective and commercially viable for the future of air travel.